|

COST & SCHEDULE CONTROL SYSTEM CRITERIA

A number of benefits are derived as a result of the criteria approach, particularly as a result of the demonstration review process, owner representatives gain a good working knowledge of contractor operations, procedures and terminology, leading to better communications with the contractor as well as inspiring greater confidence in contracto.

Objectives in using the Criteria

In an effort to obtain consistent, reliable data on the status of major system acquisitions and major projects, a number of different approaches have been instituted, ranging from complete reliance on contractors’ existing internal systems to the imposition of detailed management systems for contractors to use during the performance of contracts.

The criteria approach differs from previous efforts in that it allows contractors to use the specific management procedures of their choice, but sets forth the characteristics and capabilities which should be inherent in an effective cost and schedule control system.

The objective is twofold: first to obtain assurance that contractors internal management systems are sound, and once this is accomplished, to rely on summarized data for contract management requesting detailed data only in those areas where problems exist.

The CSCSC contain thirty-five criteria grouped into five major categories. Generally, the five sections deal with the following requirements:

1. Organization

These criteria require that the contractors system provide for clear definition of the overall contractual effort, with a work breakdown structure serving as a framework for displaying subdivisions of effort.

Integration of the work breakdown structure with the functional organization structure is required in order to provide for assignment of responsibilities for identified work tasks. Additionally, integration of the planning, scheduling, budgeting, work authorizing and cost accumulating subsystems is a key element in an effective control system.

2. Planning and Budgeting

All authorized work must be planned, scheduled, budgeted and authorized within the system. Establishment of the performance measurement baseline is the key requirement of this section.

3. Accounting

Costs of completed work must be accumulated from the levels at which costs are initially recorded to the summary level as directly as possible without need for allocations in summation. Cost of materials should be handled in such a way that the cost of work does not include cost of materials not yet on hand.

4. Analysis

Actual versus planned performance comparisons are required within this group. Thresholds for variance analyses should be established to avoid the excess effort resulting from analyzing insignificant variances.

It is particularly important that variances be examined in terms of increments or aggregations of work large enough to produce significant information. Analyzing individual work package variances, for example, should not be necessary and would probably not be cost effective, other than on an exception basis.

5. Revisions and access to Data

Incorporation of changes authorized by the project owner and due to internal replanning are dealt within this section. Particular emphasis is placed on the need to retain a meaningful performance measurement baseline.

Other requirements include reconciliation of estimated costs at completion with funds requirements reports, and provisions for access to data during systems evaluations.

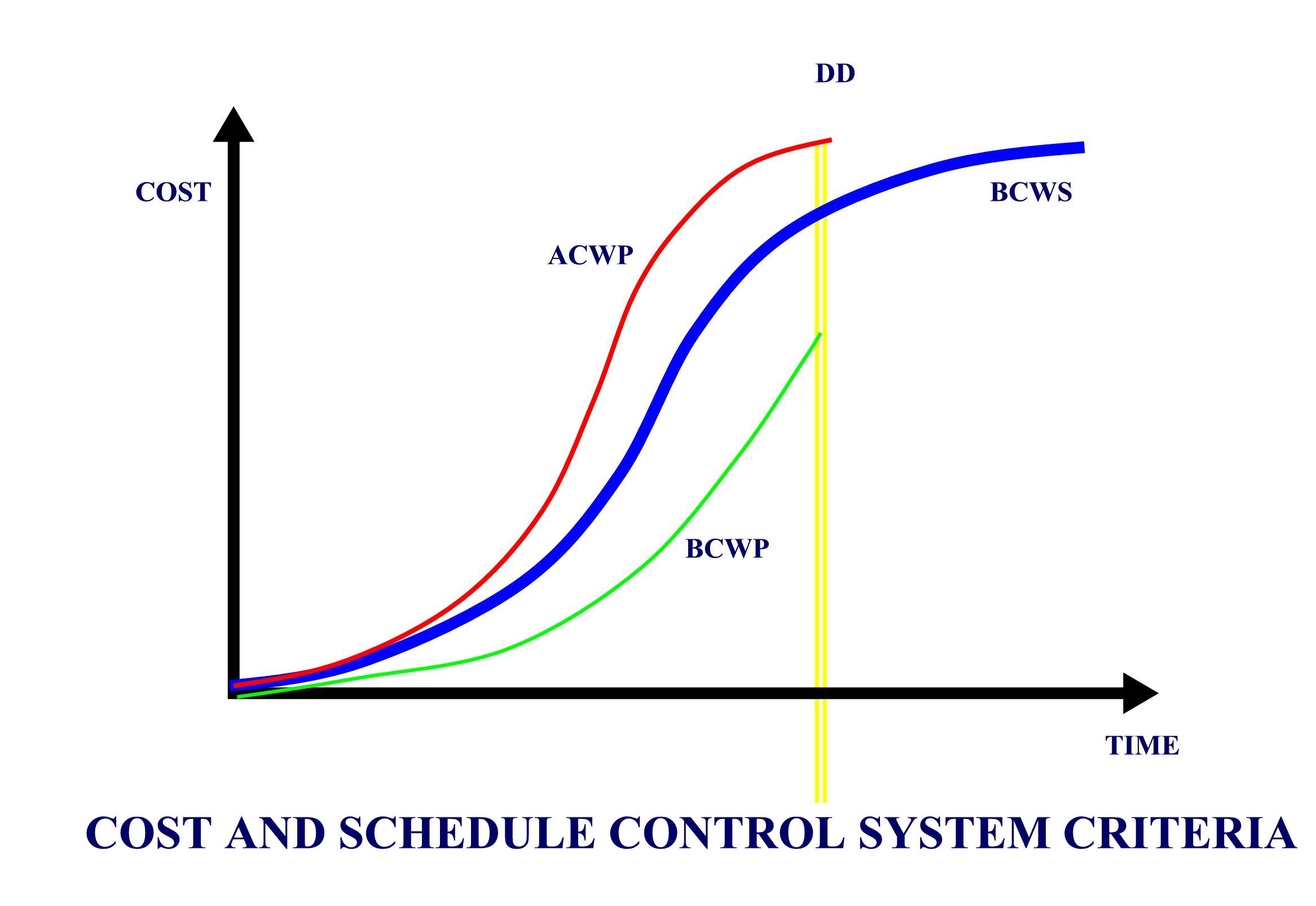

CSCSC DATA ELEMENTS

A key CSCSC data element is the Budgeted Cost Work Performed (BCWP). When compared with BCWS it provides a schedule variance. When compared with the Actual Cost of Work Performed (ACWP) it provides a cost variance.

In the foregoing example, the comparison of BCWS and BCWP resulted in an unfavorable schedule variance (-1). Also, when actual costs of work performed (35) are compared with BCWP (33), an unfavorable cost variance results (-2), showing that more money was spent than was planned for the work that has been done.

BCWS and BCWP are determined at the cost account level by adding up work package budgets. Actual costs (ACWP) may be collected directly by cost account although it is more common for costs to be collected by work packages or even in more detail.

However, all required CSCSC data elements should exist at the cost account level -- BCWS, BCWP, ACWP, schedule variance, cost variance, cost account budget and an estimated cost at completion for the cost account. This information can be used directly by cost account managers and subsequently summarized for higher levels of management and reporting to the projects owner.

It should be pointed out that unfavorable variances do not always mean poor performance by the people doing the job. The unfavorable cost variance depicted in this example could be attributable to a number of reasons.

Material costs, labor rate changes, poor initial estimates, unrealistic budgets, are other reasons which may account for poor cost performance on a particular job. The main point to be understood, though, is the cost variances can be investigated to determine their causes, and this activity is helpful in gaining a full understanding of contract performance.

The contractor should attempt to insure that any practices which might tend to suppress variances (which sometimes occur when all variances are viewed as bad) are not permitted.

The work package approach to measuring contract status for considerably more objectivity in the assessment of actual work accomplishment than many performance measurement approaches used in the past formal variance analyses and the capability to trace problems to their source, facilitate early visibility of unfavorable cost trends, and factors creating program difficulties are highlighted.

Analysis of schedule conditions in terms of cost impact is a valuable management control tool. Correlating CSCSC schedule variances with the outputs of the formal scheduling system permits a cross-check on the validity of the Budgeted Cost for Work Performed and associated cost variances.

Perhaps the most important benefit, from the owner point of view, is that contract performance is being measured against a formal, contract-related baseline, rather than against a contractor internal operating plan, which may represent something other than the contractual commitment.

|